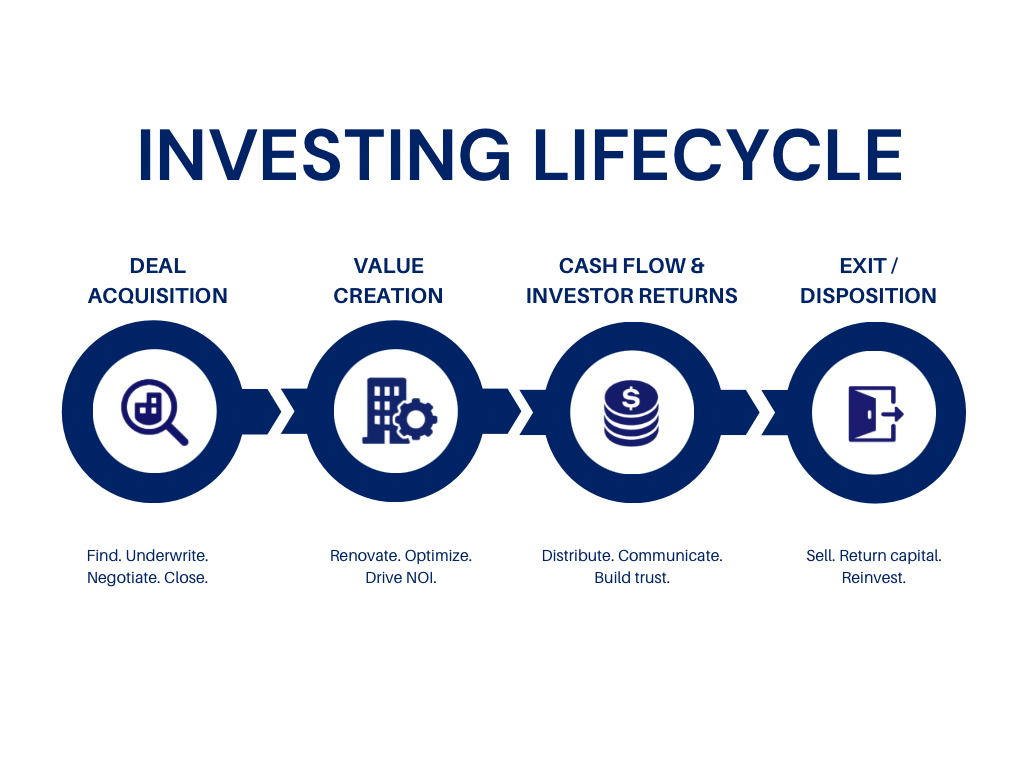

Investing in multifamly communities with asymmetric risk-return profiles to create long-term value for our stakeholders.

Asset Size

Units

Vintage

Build Year

Hold Period

Year Hold

Workforce Housing — Class B / B– / C+

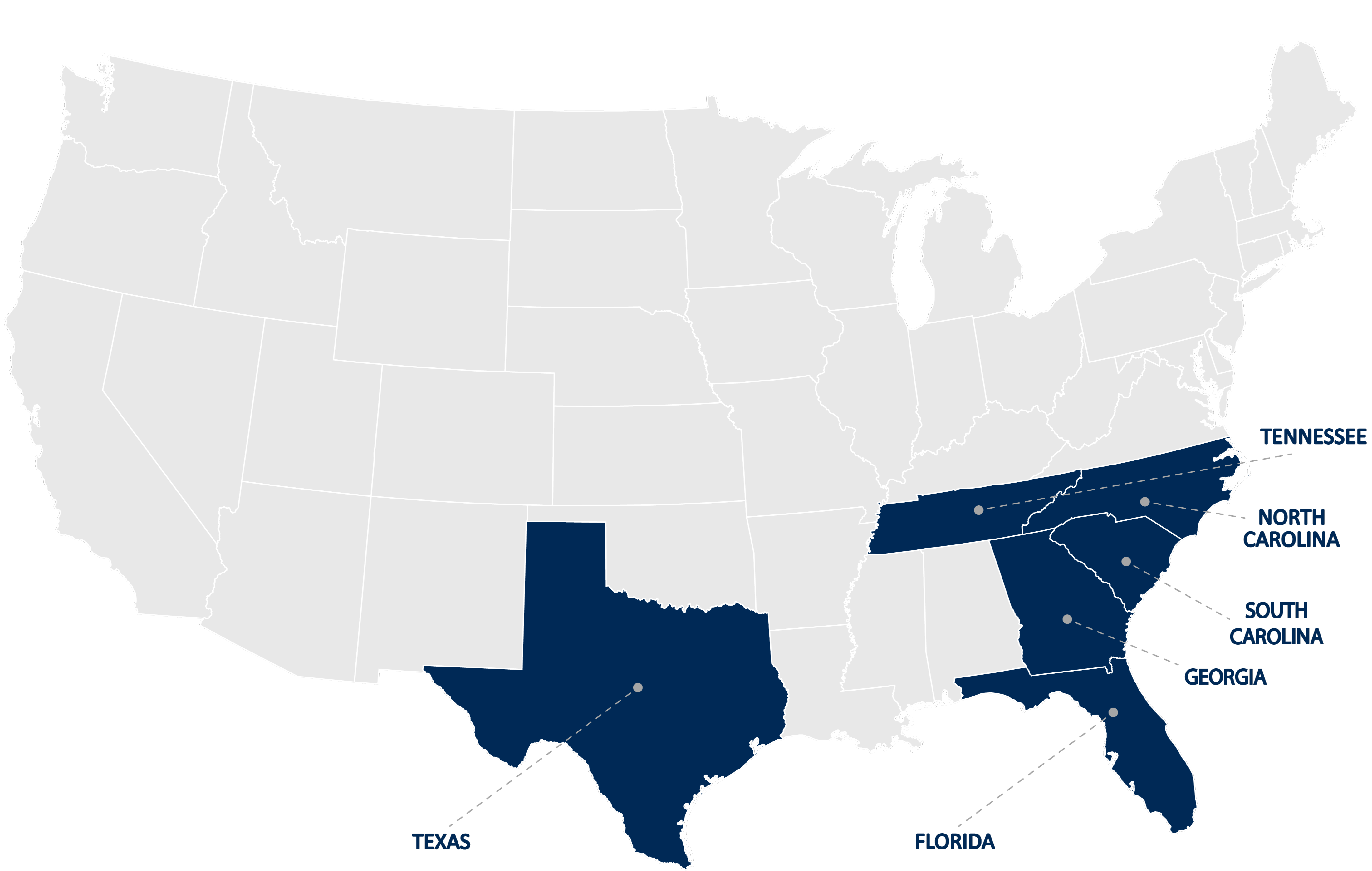

Southeast Sunbelt + Texas

Entry Basis

We pursue acquisitions only when the entry basis provides a meaningful margin of safety.

Identifiable NOI Expansion

Operational value creation must be supported by a defined operational initiative.

Stabilized Yield

Stabilized yield underwrited materially above acquisition cap rate.

Downside Scenario Modeling

All investments modeled through conservative downside scenarios.

Target Gross IRR

Target Return on Equity

Equity Multiple

Target Equity Multiple at Exit

Stabilized YOC

Stabilized Yield on Cost

Spread to Cap

Basis Points Above Entry Cap Rate

Strategy

Opportunistic · Sub-Institutional

Establishes a hard asset value floor

Meet or exceed minimum going-in cap

Strategy defined prior to acquisition

Returns must hold in downside case

Debt Maturing

Multifamily loans maturing 2026–2027 alone, originated at historic lows

Rate Shock

Loans originated during low-rate envireonment are refinancing at materially higher costs

Construction Starts

Multifamily construction starts have dropped more than 40% from 2023-2025

Deployment Target

Capital deployment objective over the next 3–5 years

Debt Maturity Wall

Over $320B in multifamily debt matures across 2026–2028; much of which originated during the low-rate era and now facing refinancing at rates nearly double that. Operators face a binary choice: refinance at economics that no longer work, or sell. Bridge borrowers who have exhausted rate cap reserves are already entering the market as motivated sellers.

Supply-Driven Compression

Record deliveries across Sunbelt markets pushed vacancy up, forced landlord concessions, and compressed NOI; dragging valuations meaningfully below replacement cost in key submarkets. High-supply markets are creating a compelling entry point for disciplined buyers. The new supply pipeline is now contracting sharply, further tightening future inventory.

Below-replacement-cost basis available across primary target markets

A window to acquire institutional-quality assets at a basis unavailable just 24 months ago.

We are deploying capital into sub-institutional assets at a basis that debt pressure and valuation compression have made structurally favorable — acquiring quality, under-optimized assets before this window normalizes. We are seeking aligned equity partners to deploy north of $50M across NC, SC, TN, GA, and TX over the next 3–5 years.

Unit Range · Class B / B– / C+ (1970+)

NC · SC · TN · GA · TX

Target Hold Period

Lever

Comprehensive lease audit on day one. Will identify every unit with loss-to-lease, building a structured burn-off schedule, and look to reprice to market on every turn.

Executed immediately post-close on 100% of units

Lever

Vendor contracts are systematically reviewed and rebid following acquisition. Procurement discipline is applied to eliminate unnecessary expense leakage.

Targeting 8–12% reduction in controllable operating expenses

Lever

Many 1970s vintage assets carry landlord-paid utilities, creating a structural inefficiency we systematically correct. Ratio Utility Billing shifts water, sewer, and trash costs to residents on a compliant, proportional basis across all target states.

Recovers $40–80 per unit / month flowing directly to NOI

Lever

A defined renovation scope executed consistently across assets, utilizing standardized materials, vendors, and timelines. This repeatable approach ensures predictable costs, controlled scope, and consistent rent premiums.

$8–12K per unit targeting $100+ / month rent premium per upgraded unit

Lever

Vacancy represents the largest cost center in multifamily operations. Structured retention programs, proactive renewal outreach, and relentless maintenance standards are implemented to minimize turnover and stabilize occupancy.

Target stabilized occupancy: 95%+

These operating levers form the core of Blackstar’s asset management approach and are applied consistently across every acquisition from day one of ownership.

Every acquisition is structured so downside is limited and upside is driven by execution.

Where Returns Come From

Multiple independent levers drive value. Each one additive, none of them dependent on macro conditions breaking in our favor.

RISK PROFLE

Where Risk Is Contained

Structural entry discipline limits loss exposure before execution even begins. Downside is bounded. Upside is not.

Stabilized yield spread above entry cap rate

Minimum DSCR underwritten at stabilized occupancy

Multiple exit pathways

Our strategy centers on acquiring Class C to B multifamily properties in Southeast markets where operational inefficiencies create measurable value-add potential.

We execute these investments alongside experienced operating partners who share our same vision. We are in process of building a repeatable acquisition platform that consistently performs as we scale.

Target markets are selected based on employment & long-term supply and demand fundamentals, among other metrics.

Primary target counties include Mecklenburg, Guilford, Gaston, and Catawba; among others.

Focus areas include Greenville, Richland, and York counties, along with select surrounding markets.

Key targets include DeKalb, Gwinnett, and Fulton counties.